Schedule 8 is a summary of all of the copies of the multiple copy form, Capital Cost Allowance (CCA) Workchart (Jump Code: 8 WORKCHART). These two forms are completely interrelated. You can access the information in the workchart at any time by double-clicking a cell in Schedule 8.

Characteristics of the Capital Cost Allowance Workchart

The CCA workchart is completely dynamic, so the display in the workchart is modified according to the selected class.

Once the class is selected, only the relevant cells will appear for calculation purposes.

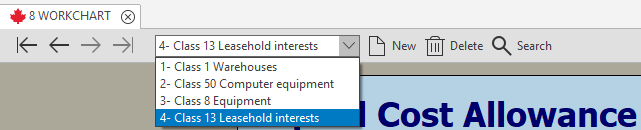

In the workchart, a drop-down menu (empty to start with) then displays the relevant information for each class created.

As a result, the following information is available for each class created:

- entry number (according to the order of creation);

- the number of the class on line 200;

Note: To enable data import into a client file and to be able to ensure a better tracking of a CCA class that can have various CCA rates as a result of an additional CCA deduction, we have added a letter at the end of the number of the prescribed class to differentiate them. It consists of classes 1a at 10% (4% + 6%) and 1b at 6% (4% + 2%). Note that when paper printing all of the schedules that require a CCA class number, a custom class with a letter will be displayed, while when printing the schedules in “T2 - Bar codes” format and during electronic transmission of the federal return and the RSI schedules for Alberta requirements, the corresponding prescribed class number will continue being used.

- the description given to this class in the appropriate cell.

- the “Québec” reference, in cases of a separate class that is used solely for the Québec income tax return and that relates to property qualifying for the additional CCA of 30%, the indicator “Québec.”

Below is an example of what the drop-down menu in the CCA workchart could look like.

The classes are listed in the drop-down menu for line 200 and, according to the selected class, one of the following four data entry screens displays to calculate the CCA:

- CCA class 10.1;

- CCA class 13;

- CCA class 14;

- CCA other than classes 10.1, 13 and 14.

Numerous classes are available in the drop-down menu for line 200. All of these classes are divided into five groups according to the display that will automatically be available when a class is selected.

Thus, class 10.1 includes passenger vehicles; class 13 includes leaseholds, class 14 includes patents, franchises, concession or licences, and classes 24, 27, 29 and 34 are for property that is generally used for manufacturing and processing. All other classes are part of a general group that will not change the original display of the workchart.

Linking a CCA Class to a Statement of Real Estate Rental Properties (Regulation 1100(11))

Steps for linking a CCA class to a statement of real estate rental property

A copy of the Statement of Real Estate Rental Property must be completed for each rental property that the corporation possesses either as a sole owner or as a co-owner.

Then indicate that you want to link this property to a statement of real estate rental property by answering the relevant question, and then, using the drop-down menu, select the address of the property for which you wish to transfer the information:

Consequently, all information relating to the calculation of the class will be transferred to the “Calculation of capital cost allowance (CCA)” section of the selected rental form and the program will be able to recalculate the CCA based on the limitations for rental properties under regulation 1100(11).

This new CCA claim will be updated to Schedule 8, Capital Cost Allowance (CCA) (Jump Code: 8) as well as to the T2 - Bar Code return.

The calculated federal CCA claim is automatically updated to the Québec and Alberta CCA columns in the CCA workchart. Override the provincial information if it differs from the federal.

CO-771, Calculation of the Income Tax of a Corporation (Jump Code: 771)

When, in the Capital Cost Allowance (CCA) Workchart (Jump Code: 8 WORKCHART), the CCA amount claimed with regard to rental properties for Québec purposes differs from the amount claimed for federal purposes, a diagnostic prompt you to review the income (or loss) amount from properties calculated for Québec purposes on line 22, if applicable.

Data rolled forward

The real estate rental property will remain linked to a statement of real estate rental property until you answer Yes to the question Was this the final year of your rental operation? in the Statement of Real Estate Rental Properties (Jump Code: RENTAL).

Sorting of CCA classes

Two sort functions are available in this schedule. When you click the first ![]() button, the CCA classes will appear in an ascending order on their class number, both on screen and when printing. If the same class number is found twice or more, a second sort will automatically be performed: items from a same category will be classified in alphabetical order according to information in the Description column. When adding classes, you will have to repeat the process to sort them. In addition, when you click the second

button, the CCA classes will appear in an ascending order on their class number, both on screen and when printing. If the same class number is found twice or more, a second sort will automatically be performed: items from a same category will be classified in alphabetical order according to information in the Description column. When adding classes, you will have to repeat the process to sort them. In addition, when you click the second ![]() button, the CCA classes will appear in an ascending order on their capital cost allowance (CCA) rate, both on screen and when printing. If the same CCA rate is found twice or more, a second sort will automatically be performed: items from a same CCA rate will be classified in an ascending on their Class number column. If the same class number is found twice or more, a third sort will automatically be performed: items from a same category will be classified in alphabetical order according to information in the Description column. When adding classes, you will have to repeat the process to sort them.

button, the CCA classes will appear in an ascending order on their capital cost allowance (CCA) rate, both on screen and when printing. If the same CCA rate is found twice or more, a second sort will automatically be performed: items from a same CCA rate will be classified in an ascending on their Class number column. If the same class number is found twice or more, a third sort will automatically be performed: items from a same category will be classified in alphabetical order according to information in the Description column. When adding classes, you will have to repeat the process to sort them.

Note that the ![]() buttons will also be on the Forms CO-130.A, Capital Cost Allowance (Jump Code: Q8) and the Alberta Schedule 13, Capital Cost Allowance (Jump Code: A13). Any sort requested from one of these three forms will automatically be applied to the two other forms.

buttons will also be on the Forms CO-130.A, Capital Cost Allowance (Jump Code: Q8) and the Alberta Schedule 13, Capital Cost Allowance (Jump Code: A13). Any sort requested from one of these three forms will automatically be applied to the two other forms.

Capital Cost Allowance Claim Defaulted to Zero for all Classes

A check box allows you to cancel the default CCA calculation for all classes. Note that terminal losses, recapture of capital cost allowance and any overrides made on the CCA claimed will not be modified when the box is selected.

This check box will also be on Form CO-130.A, Capital Cost Allowance (Jump Code: Q8) and the Alberta Schedule 13, Alberta Capital Cost Allowance (CCA) (Jump Code: A13). The box appearing on the provincial forms will be selected according to federal Schedule 8, but it will be possible to make a separate election by overriding it.

Additions in the year (line 203)

The available-for-use rule determines the earliest tax year in which a corporation can claim CCA for depreciable property.

The property must be listed as an acquisition in the year (line 203) in a given class for CCA purposes only in the tax year where it is available for use based on the available-for-use rule.

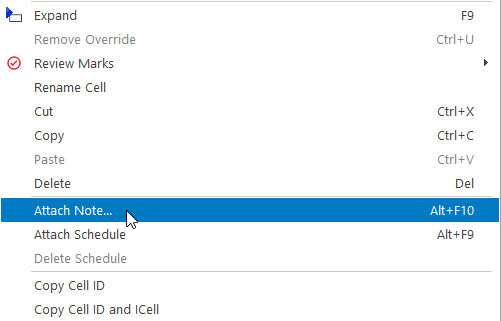

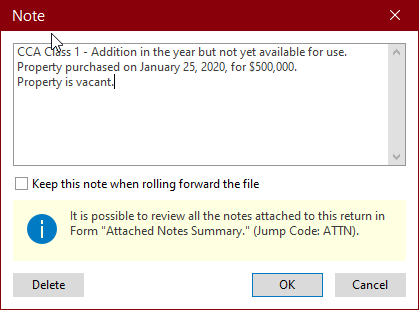

To remember to list a property that is not yet available for use, we suggest that you attach a note to the relevant line 203 on which you should enter as much information as possible.

You can keep this note when rolling forward the client file by selecting both the box Keep this note when rolling forward the file, in the Note dialog box, and the box Keep the notes attached to cells, under Options and Settings/Roll Forward/Data Options.

Example:

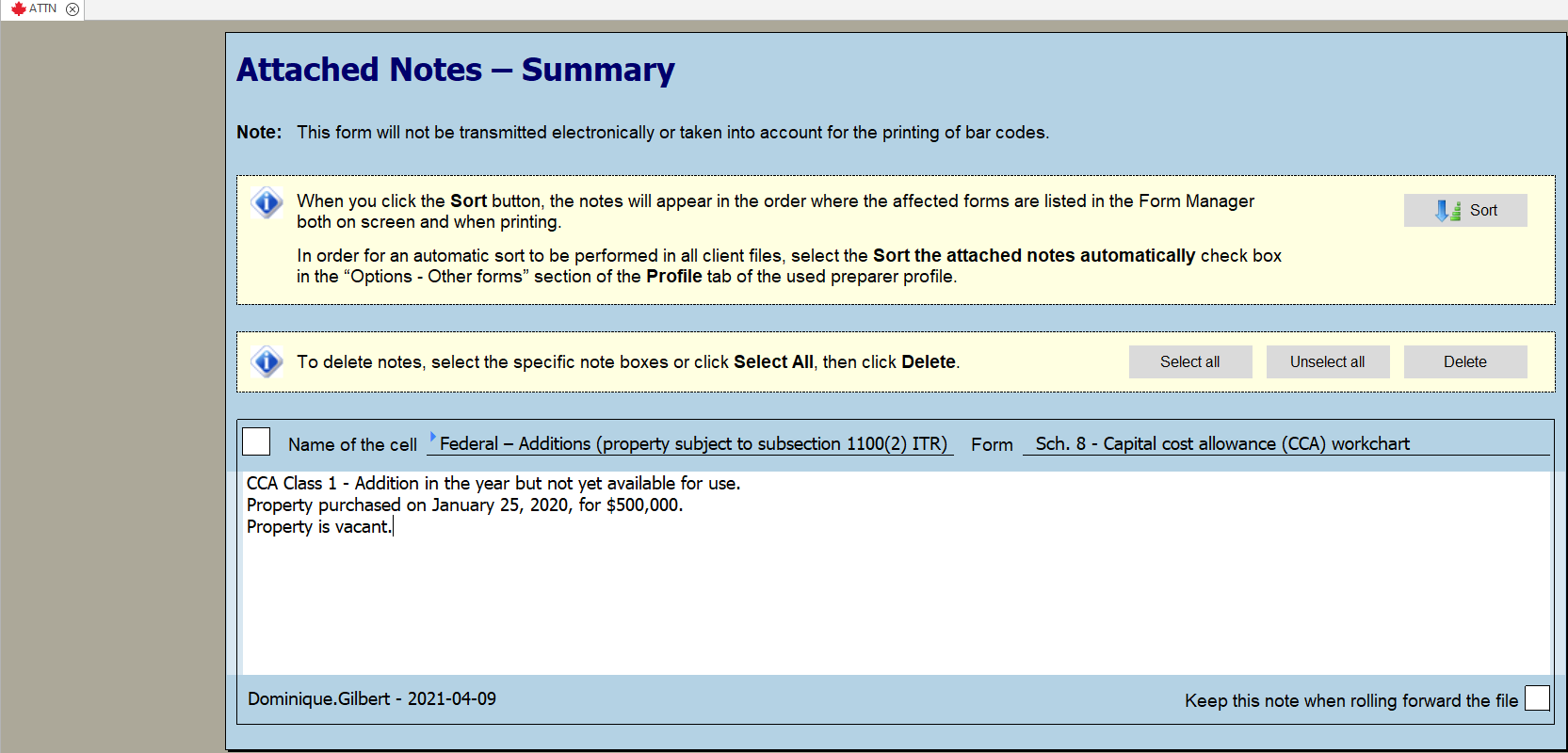

The content of the note can be consulted at any time by placing your cursor on line 203 of the appropriate class or by accessing the Attached Notes – Summary (Jump Code: ATTN).

For more details on how to use attached notes, consult the “Attached Notes and Schedules” Help topic.

Adjustments and transfers (lines 205)

In Schedule 8 WORKCHART, several separate lines have been created to help identify the adjustment type that is affecting the CCA class. The amounts entered on all these lines (including lines 221 and 222) aggregate the amount shown on line 205, Adjustments and transfers, in column 5 of Schedule 8.

ITC (prior year)

This line can be used to enter the federal investment tax credits (ITCs) (other than research and development ITCs) used to reduce tax payable or claimed as a refund in the previous tax year. It can also be used to enter any provincial or territorial ITCs received or entitled to be received by the corporation in the current year.

GST/PST rebate

This line can be used to enter the goods and services tax/harmonized sales tax (GST/HST) credit relating to property in a class, and any provincial sales tax (PST) credit, where applicable, claimed or entitled to be claimed, or the rebate received or entitled to be received by the corporation in the year.

Adjustments and transfers not affecting the adjustments under subsection 1100(2) ITR

The amount on the line can be used to deduct, among other things, the amount of the capital cost reduction of the class resulting from the application of section 80 ITA as well as the government assistance received or entitled to be received in the year with respect to property in the class.

The amount on the line can also be used to add, among other things, the value of depreciable property transferred as a result of the amalgamation or winding-up of a subsidiary or in accordance with section 85 ITA, rebates of sales tax (provincial or federal) or GST/HST input tax credits with respect to property in the class as well as the government assistance amount repaid in the year that previously reduced the capital cost of the class;

Line 221, Assistance received or receivable during the year for a property after its disposition and line 222, Amount repaid during the year for a property after its disposition

The amounts entered on these lines are included in the calculation of the lines relating to the UCC adjustment under subsection 1100(2) of the Income Tax Regulations.

This measure provides that the capital cost of eligible depreciable property acquired after April 18, 2021, and that becomes available for use before January 1, 2024, by a Canadian-controlled private corporation (CCPC) may be deducted entirely, up to a limit of $1.5 million per taxation year. The limit must be allocated among eligible persons and partnerships that are members of an associated group. The limit allocated is also prorated for taxation years that are shorter than 51 weeks. Note that the unused limit cannot be carried forward. The half-year rule is suspended for property eligible for this measure.

Eligible property is depreciable property subject to the CCA rules, other than property included in CCA classes 1 to 6, 14.1, 17, 47, 49 and 51.

A CCPC which, in a taxation year, puts into use eligible property with a capital cost that exceeds the allocated limit may decide to which CCA class immediate expensing is allocated to. Then, the excess capital cost is subject to the regular CCA rules for each class. Eligible property that is also an AIIP in CCA classes 43.1., 43.2 and 53 or a ZEV in classes 54 to 56 that already qualify for an enhanced CCA rate of 100% will not reduce the maximum amount available.

Calculation of line 238, Immediate expensing

In Schedule 8 WORKCHART (Jump Code: 8 WORKCHART), the amount calculated on line 238, Immediate expensing, depends on the capital cost of the eligible property that became available for use in the taxation year entered on line 236, DIEP UCC. This line is calculated from lines 232, Cost of additions for designated immediate expensing property (DIEP) included in the amount on line 203, to which is added the amount on line Adjustments relating to DIEP included on line 205 and from which the amount on line 234, Proceeds of disposition of DIEP included on line 207, is deducted.

Note: For a property that is acquired (or becomes available for use) in the current taxation year, is designated as a DIEP and is disposed of in the same taxation year, add the proceeds of disposition on both line 207 and line 234. Otherwise, for a property that was designated as a DIEP in a prior taxation year and is disposed of in the current taxation year, add the proceeds of disposition only on line 207.

Line 232, Cost of additions for designated immediate expensing property (DIEP) included in the amount on line 203, is calculated in the following situations:

- For a CCA class 10.1, when the answer to the custom question Is the property a designated immediate expensing property (DIEP) for the taxation year? is Yes and the Acquisition date is, in the taxation year, after April 18, 2021, and before January 1, 2024, the amount corresponds to the limit amount calculated based on the Purchase cost;

- For a CCA class 13, when the taxation year start date is after April 18, 2021, and before January 1, 2024, the amount corresponds to the total of the amount entered on lines 203;

- For a CCA class 14, when the Date of acquisition is, in the taxation year, after April 18, 2021, and before January 1, 2024, the amount corresponds to the amount entered on line 203;

- For other CCA classes:

- When Form Additions and Dispositions Workchart (Jump Code: 8 WORKCHART ADD) is used, the amount corresponds to the total of the Adjusted capital cost of properties for which the Acquisition date is, in the taxation year, after April 18, 2021, and before January 1, 2024, and the answer to the custom question Is the property a designated immediate expensing property (DIEP)? is Yes;

- When Form 8 WORKCHART ADD is not used and the taxation year start date is after April 18, 2021, and before January 1, 2024, the amount corresponds to the total of the amount entered on lines 203;

Note that the calculation is not made for a CCA class with a CCA rate of 100%, nor for a CCA class with an enhanced CCA rate of 100%.

When the total capital cost of eligible property exceeds the corporation’s allocated limit, the program allocates the latter amount, up to the cost of eligible additions and the UCC balance, whichever is less, in the following order:

- Classes other than classes 13 and 14, with eligible property in increasing order of the CCA rate. For classes with eligible property that are linked to the RENTAL form (Jump Code: RENTAL), the amount is also limited by the net income before capital cost allowance;

- Class 13;

- Class 14.

Property in CCA classes 24, 27, 29 and 34 are not considered in the calculation of the amount on line 238, Immediate expensing. In addition, for the purposes of calculating the amount on line Immediate expensing in the Québec column, eligible property in separate CCA classes 14, 44 and 50 created to apply specific accelerated depreciation rules in Québec that qualify for an enhanced CCA rate of 100% are also not taken into account.

The amount entered on line 238, Immediate expensing, is subtracted from line Remaining UCC that is used to calculate line 224, UCC adjustment for other property acquired during the year and line Net capital cost additions of AIIP and ZEV acquired during the year in combination with line Cost of acquisitions for property other than DIEP and line 225, Cost of acquisitions that are AIIP and ZEV (other than DIEP).

When the remaining limit is not sufficient to cover the cost of eligible additions, the remaining amount is applied to the capital cost of eligible property acquired in the taxation year in the following order:

- Non-AIIP subject to subsection 1100(2) ITR;

- AIIP.

Table Agreement between associated eligible persons or partnerships (EPOPs) (Part 1 of Schedule 8)

This table allows you to allocate the limit between the persons and partnerships of an associated group. For associated corporations, the information in the Name of EPOP, Business number, Percentage assigned under the agreement and Limit Allocated columns is updated from Schedule 9 WORKCHART (Jump Code: 9 WORKCHART) when the answer to the question Is the corporation an eligible corporation for immediate expensing? is Yes in the Schedule 8 – Capital Cost Allowance (CCA) section of Schedule 9 WORKCHART. Use the Add button to add lines to manually enter the information for associated eligible individuals and partnerships. The limit allocated in the Alberta column is equal to the limit allocated in the Federal column. For the limit allocated for Québec purposes, see Form TP-130.EN, Immediate Expensing Limit Agreement (Jump Code: Q8EN).

Form CO-130.AD, Capital cost allowance for designated immediate expensing property (Jump Code: Q8AD)

This Québec form allows you to enter the information regarding the designated immediate expensing property (Part 2) and calculate the immediate expensing amount deducted (Part 3) for the taxation year.

For a CCA class entered in Schedule 8 WORKCHART, when the property is entered in Schedule 8 WORKCHART ADD and the answer to the custom question Is the property a designated immediate expensing property (DIEP)? is Yes, a line with the relevant information is automatically created in the table in Part 2. Otherwise, when an amount is entered on line Cost of additions for designated immediate expensing property (DIEP) included in the amount on line 203 in the Québec column, a line will be created with the number of the CCA class in column D and the capital cost in column E, and you will need to complete the rest of the information for the line and/or create other lines using the Add button if this amount corresponds to the capital cost of more than one property.

The table in Part 3 will fill out automatically based on the data entered on the corresponding lines in Schedule 8 WORKCHART when there is an amount on line Cost of additions for designated immediate expensing property (DIEP) included in the amount on line 203 under the Québec column.

As per Revenu Québec requirements, a copy of Schedule 8 must be filed with the Québec tax return.

When the corporation has a permanent establishment in Québec and Form TP-130.EN (Jump Code: Q8EN) is applicable:

- A copy of this schedule is automatically attached to the Québec return when this return is electronically filed; and

- A copy of this schedule is printed for the Québec return with the “Client,” “GOVT RSI, Bar Codes,” and “Office” print formats.

Data calculated to manage the information relating to property acquired before January 1, 2017

Deemed total capital cost of property in the class under paragraph 13(38)(a) ITA (line K)

This amount will be calculated based on the following formula:

(4/3 x [G + (3/2 x H) + I + J])

where

G is the CEC balance in respect of the business on January 1, 2017

H is the amount that would need to be included in income pursuant to paragraph 14(1)(b) ITA, as that paragraph applied immediately before January 1, 2017, when the CEC balance is negative.

I is the total of the deductions that reduced the CEC in respect of the business for taxation years ending before January 1, 2017.

J is item D.1 of the CEC definition set out in paragraph 14(5) ITA, as that paragraph applied immediately before January 1, 2017, when the CEC balance is negative.

Amount deemed allowed as a deduction against the capital cost of property in the class under paragraph 13(38)(c) ITA for taxation years ending before January 1, 2017 (Line L)

The deemed CCA allowed is equal to the difference between the deemed total capital cost and the positive CEC balance at the time of the roll forward.

UCC balance in the class on January 1, 2017 (Line M)

The UCC balance is equal to the difference between the deemed total capital cost and the deemed CCA allowed. Any positive result obtained also corresponds to the UCC balance (opening) entered on line 201, if this amount is positive. In general, the UCC balance at the time the class is created will be equal to the CEC balance in respect of the business (line G).

CCA claimed with respect to this UCC balance in preceding taxation years (Line N)

This is the total amount of the capital cost allowance (CCA) and the additional deduction that has been deducted from the UCC balance in the class on January 1, 2017 (line M), for taxation years ending between January 1, 2017, and December 31, 2026. This amount will be calculated each year when the client file is rolled forward.

The amount updated to this line will vary according to the CCA claimed. When rolling forward a client file, the program will automatically add to the amount entered on the line in the initial client file, the lesser of:

- the total of the CCA and the additional deduction calculated for the UCC balance on January 1, 2017, net of the CCA amount claimed with respect to this UCC balance in prior years; and

- the CCA amount claimed on line 217 for the class.

When the CCA amount claimed on line 217 of the form is not nil and it is different from the maximum CCA that can be claimed by the corporation, verify if the amount updated is correct.

Additional deduction

For taxation years ending before 2027, an additional deduction corresponding to 2% of the UCC in the class on January 1, 2017, can be claimed with respect to property of a business that has been acquired before January 1, 2017. This additional deduction is, however, reduced from any amount that has been deducted in prior taxation years and three times the total of the amounts deducted from the UCC because of the amounts received to which subsection 13(39) ITA applies.

Furthermore, if the total of that additional deduction and the eligible CCA for the year is less than $500, the additional deduction may be increased to allow a total CCA of $500, without exceeding the UCC in the class on January 1, 2017 (net of CCA deductions for prior years that started after January 1, 2017), or to ensure that the CCA in respect of the class for the year to be more than the UCC balance (before the application of such deduction).

Based on CRA requirements, when property acquired during the year is included in CCA class 43.1 or 43.2 on line 203, additional information is required with respect to each of these acquisitions. This information is used for statistical purposes only.

Therefore, a section has been added to the Capital Cost Allowance (CCA) Workchart (Jump Code: 8 WORKCHART), for these two CCA classes only. This section displays when an acquisition amount is entered on line 203 for property in class 43.1 or 43.2. It includes multi-lines areas that allow you to provide the information required for each of the property acquisitions included in one of these classes. Follow the instructions below to complete the section:

- Column 301, Type of asset code: Choose the most appropriate code from a list of 20 codes provided by the CRA. See the complete list of these codes and related definitions below.

- Column 302, Province where the asset is located: By default, the program determines the province where the corporation’s head office (corporation’s head office – provincial or territorial jurisdictions of Canada only) is located based on information indicated on line 016 of Form Identification (Jump Code: ID). Validate the province determined by the program and change it if applicable.

- Column 303, Percentage allocated to the asset: Indicate the percentage of each property acquisition with relation to the total amount of property acquisitions during the year (line 203) for the given class (43.1 or 43.2). The total of the percentages allocated to the property in a class must be equal to 100%.

Note that the CRA does not want to add these lines on its Schedule 8. This is why this information is not found on the paper copy of Schedule 8; it appears on screen only. However, this information is mandatory: it is included in the bar codes and is transmitted electronically.

Line 301 - Type of asset code and definition

Note: The federal government proposes to expand the eligibility criteria for CCA classes 43.1 and 43.2 to include several clean energy generation equipment acquired and that became available for use in the tax year after April 18, 2021. For more information, consult the Capital cost allowance for clean energy equipment section in Appendix 6 of the 2021 federal budget.

|

Codes |

Description |

Definition |

|

Code 01 |

Cogeneration systems |

Cogeneration systems include certain equipment that is part of a system that is used to generate electricity only, or electricity and useful heat from eligible fuels or thermal waste. Eligible fuels include fossil fuels (i.e., petroleum, natural gas or related hydrocarbons, basic oxygen furnace gas, blast furnace gas, coal, coal gas, coke, coke oven gas, lignite, peat, or solution gas), eligible waste fuels (e.g., biogas, bio-oil, digester gas, landfill gas, municipal waste, plant residue, pulp and paper waste, wood waste), producer gas, or spent pulping liquor. Fossil-fuelled cogeneration systems that become available for use after 2024 will not qualify for Classes 43.1 and 43.2. |

|

Code 02 |

Waste-fuelled electrical generation equipment |

Waste-fuelled electrical generation equipment includes certain equipment where the equipment is part of a system that is used to generate electricity or, in the case of cogeneration systems, electricity and useful heat using eligible waste fuels (e.g., biogas, bio-oil, digester gas, landfill gas, municipal waste, plant residue, pulp and paper waste, wood waste), fossil fuel, producer gas, or spent pulping liquor. Specified waste-fuelled electrical generation systems that become available for use after 2024 and that use fuel of which more than 25% of the energy content is from fossil fuel, determined on an annual basis, will not qualify for Classes 43.1 and 43.2. Eligibility for Classes 43.1 and 43.2 for specified waste-fuelled electrical generation systems that become available for use after 2024 will be subject to a heat rate threshold. |

|

Code 03 |

Thermal waste electrical generation equipment |

Thermal waste electrical generation equipment includes equipment that is used to generate electrical energy in a process where all or substantially all of the energy input is thermal waste. |

|

Code 04 |

Wind energy conversion systems |

Wind energy conversion systems include fixed location equipment that is used primarily for the purpose of converting wind energy into electrical energy. |

|

Code 05 |

Small-scale hydro-electric installations |

Small-scale hydro-electric installations include hydro-electric generating installations with a rated capacity at the installation site of 50 megawatts (MW) or less. |

|

Code 06 |

Fuel cell equipment |

Fixed location fuel cell equipment includes property used to generate electrical energy or electrical energy and heat from hydrogen by the electrochemical reaction of hydrogen and oxygen. Eligible fuel cell equipment uses oxygen in the air and hydrogen generated from:

|

|

Code 07 |

Photovoltaic equipment |

Photovoltaic electrical generation equipment includes fixed location photovoltaic equipment that is used primarily for the purpose of generating electrical energy from solar energy. |

|

Code 08 |

Water-current, tidal or wave energy equipment |

Water-current, tidal or wave energy equipment includes equipment that is used primarily for the purpose of generating electrical energy from the kinetic energy of flowing water, tidal currents or wave energy. |

|

Code 09 |

Geothermal energy equipment |

Geothermal electrical generation equipment includes equipment used primarily for the purpose of generating electrical energy solely from geothermal energy. |

|

Code 10 |

Active solar heating equipment |

Active solar heating equipment includes property that is used primarily for the purpose of heating an actively circulated liquid or gas. It refers to equipment that uses a liquid or gas to transfer heat - collected from solar energy in solar collectors - to water heaters or solar energy conversion equipment. |

|

Code 11 |

Ground source heat pump systems |

Ground-source heat pump systems includes property that is used primarily for the purpose of heating an actively circulated liquid or gas by using the ground as a solar energy collector and a heat pump to extract and convert thermal energy from the ground into useful heat. |

|

Code 12 |

District energy equipment |

District energy equipment includes equipment that is part of a district energy system that is used primarily to provide heating or cooling from a central thermal energy generation unit to one or more buildings. The thermal energy is primarily generated by: an eligible cogeneration system, active solar heating equipment, a ground-source heat pump system, a heat recovery equipment or waste fuelled thermal energy equipment. |

|

Code 13 |

Waste-fuelled heat production equipment |

Waste-fuelled heat production equipment includes equipment used solely for the purpose of generating heat energy, primarily from the consumption of eligible waste fuel (i.e., biogas, bio-oil, digester gas, landfill gas, municipal waste, plant residue, pulp and paper waste or wood waste) or producer gas. The remaining fuel energy input may be from fossil fuels. Waste-fuelled heat production equipment that becomes available for use after 2024 and that uses fuel of which more than 25% of the energy content is from fossil fuel, determined on an annual basis, will not qualify for Classes 43.1 and 43.2. |

|

Code 14 |

Heat recovery equipment |

Heat recovery equipment includes equipment that is used primarily for the purpose of conserving energy or reducing the requirement to acquire energy and that recovers thermal waste generated by an eligible electrical generation or cogeneration system, or an industrial process. |

|

Code 15 |

Landfill gas/digester gas collection equipment |

Landfill gas and digester gas collection equipment includes equipment used primarily for the purpose of collecting landfill gas or digester gas. |

|

Code 16 |

Liquid biofuel production systems |

Liquid biofuel production systems include equipment all or substantially all of the use of which is to produce liquid biofuel from specified waste material or carbon dioxide. |

|

Code 17 |

Biogas production systems |

Biogas production systems include equipment that is primarily used to produce biogas by anaerobic digestion of specified waste material. These systems also include equipment that is primarily used to store biogas. |

|

Code 18 |

Enhanced combined cycle systems |

Enhanced combined cycle systems include equipment of a combined cycle process where at least 20 percent of the heat input to the process is recovered from the thermal waste of a natural gas compressor system. The recovered heat input to the system must be used to enhance the generation of electrical energy. Enhanced combined cycle systems that become available for use after 2024 will not qualify for Classes 43.1 and 43.2. |

|

Code 19 |

Expansion engine system |

Expansion engine systems include certain expansion engines, with one or more turbines, or cylinders, that are used to convert the compression energy in pressurized natural gas into shaft power that generates electricity. |

|

Code 20 |

Producer gas generating equipment |

Producer gas generating equipment includes equipment that is part of a system that generates producer gas (other than producer gas that is to be converted into liquid fuels or chemicals) primarily from eligible waste fuel or specified waste material using a thermo-chemical conversion process. Producer gas generating equipment that becomes available for use after 2024 and that uses feedstock of which more than 25% is fossil fuel when measured in terms of energy content (expressed as a higher heating value of the feedstock), determined on an annual basis, will not qualify for Classes 43.1 and 43.2. |

|

Code 20 |

Gasification equipment |

Budget 2014 proposes to include property used to gasify eligible waste fuel (i.e., biogas, bio-oil, digester gas, landfill gas, municipal waste, plant residue, pulp and paper waste or wood waste) for other applications (e.g., to sell the producer gas for domestic or commercial use). Eligible gasification property will include equipment used primarily to produce producer gas. |

|

Code 21 |

Electric vehicle charging equipment |

Electric vehicle (EV) charging equipment includes EV charging stations (EVCS) that meet certain power capacity thresholds and other electrical equipment used to supply power to those EVCS provided that:

EVCS that supply more than 10 kilowatts of power are eligible for inclusion in Class 43.1. EVCS that supply at least 90 kilowatts of power are eligible for inclusion in Class 43.2. Other electrical equipment used in connection with EVCS that supply more than 10 kilowatts of power is eligible for inclusion in Class 43.1. Other electrical equipment used in connection with EVCS that supply at least 90 kilowatts of power is eligible for inclusion in Class 43.2 even if that other electrical equipment also supplies power to other EVCS that supply more than 10 kilowatts of power. |

|

Code 22 |

Electric energy storage equipment |

Electrical energy storage equipment includes equipment that is used primarily for the purpose of storing and discharging electrical energy. If the electrical energy to be stored is generated by equipment included in Class 43.2, the electrical energy storage equipment is eligible for inclusion in Class 43.2. If the electrical energy to be stored is generated by equipment included in Class 43.1, the electrical energy storage equipment is eligible for inclusion in Class 43.1. Stand-alone electrical energy storage equipment is eligible for inclusion in Class 43.1 provided it has a roundtip efficiency greater than 50%. |

|

Code 25 |

Pumped hydroelectric energy storage |

Pumped hydroelectric energy storage includes equipment all or substantially all of the use of which is to store electrical energy. If the electrical energy to be stored is generated by equipment included in Class 43.2, the pumped hydroelectric energy storage equipment is eligible for inclusion in Class 43.2. If the electrical energy to be stored is generated by equipment included in Class 43.1, the pumped hydroelectric energy storage equipment is eligible for inclusion in Class 43.1. Stand-alone pumped hydroelectric energy storage equipment is eligible for inclusion in Class 43.1 provided it has a roundtrip efficiency greater than 50%. |

|

Code 26 |

Solid biofuel production systems |

Solid biofuel production systems include equipment all or substantially all of the use of which is to produce solid biofuel from specified waste material. Electrolytic hydrogen productin systems include equipment all or substantially all of the use of which is to produce hyrogen through electrolysis of water. |

|

Code 27 |

Equipment used to produce hydrogen by electrolysis of water |

Electrolytic hydrogen production systems include equipment all or substantially all of the use of which is to produce hydrogen through electrolysis of water. |

|

Code 28 |

Hydrogen refuelling equipment |

Hydrogen refuelling equipment includes equipment used to dispense hydrogen for use in automotive equipment powered by hydrogen. |

|

Code 29 |

Air-source heat pump systems |

Budget 2022 proposes to include air-source heat pumps primarily used for space or water heating. |

There are three CCA classes for zero-emission equipment that become available for use before 2028:

- class 54 (CCA rate of 30%) for zero-emission motor vehicles and passenger vehicles, that would be included in class 10 or class 10.1;

- class 55 (CCA rate of 40%) for zero-emission vehicles, that would be included in class 16; and

- class 56 (CCA rate of 30%) for zero-emission equipment and vehicles, that are not included in CCA classes 54 and 55.

These three CCA classes benefit from a temporary enhanced first-year CCA rate of 100% applicable to eligible zero-emission automotive equipment and vehicles that are acquired after March 18, 2019, (after March 1, 2020, for CCA class 56) and that become available for use before 2024. The enhanced rate is reduced to 75% after 2023 and before 2026 and to 55% after 2025 and before 2028.

A “zero-emission passenger vehicle” is an automobile (as defined in the ITA) that is included in class 54. For each vehicle included in class 54 that is available for use in the taxation year, a limit for the eligible capital cost (plus the sales taxes applicable on this amount) is applied as follows:

|

Acquisition Date |

Limit (before GST and PST, or HST) |

|---|---|

|

Before January 1, 2022: |

$55,000 |

|

Before January 1, 2023: |

$59,000 |

|

After December 31, 2022: |

$61,000* |

* At the date of publication of the program, the CRA informed us that the increased ceiling would only be considered once a bill confirming this increase is tabled. For Québec income tax purposes, Revenu Québec has confirmed that the ceiling is applicable.

In addition, where the vehicle is disposed of to a person or partnership with which the taxpayer deals at arm’s length,

- if the disposition occurs before July 30, 2019, the actual proceeds of disposition are multiplied by the ratio corresponding to the capital cost of the vehicle divided by the actual cost of the vehicle;

- in other cases, the actual proceeds of disposition are multiplied by the ratio corresponding to the capital cost of the vehicle divided by the result of the following formula:

D + (E + F) – (G + H)

where

D is the cost to the taxpayer of the vehicle,

E is the amount determined under paragraph 13(7.1)(d) ITA in respect of the vehicle at the time of disposition,

F is the maximum amount determined for C in the UCC definition set out in subsection 13(21) ITA in respect of the vehicle,

G is the amount determined under paragraph 13(7.1)(f) ITA in respect of the vehicle at the time of disposition, and

H is the maximum amount determined for J in the UCC definition set out in subsection 13(21) ITA in respect of the vehicle.

When the Additions and Dispositions Workchart is used, the program calculates the eligible capital cost of a zero-emission passenger vehicle in the year of acquisition as well as the proceeds of disposition in the year of disposition when you complete the “Information relating to zero-emission vehicles” section. The field “Government assistance received or repaid” located in the “Disposition of a zero-emission passenger vehicle” subsection should be used to enter the result obtained according to the portion (E + F) – (G + H) of the formula described above to allow for the calculation of the proceeds of disposition when the disposition is made after July 29, 2019.

Property included in classes 54, 55 and 56 are not AIIP and the half-year rule does not apply to them. However, note that, for the purposes of the calculations in Schedule 8, the CRA considers property in these classes acquired in the taxation year to be AIIP.

Subsection 1103(2j) of the Regulations provides the corporation the ability to opt-out of class 54, 55 or 56 treatment and instead include the relevant property in its otherwise applicable CCA class. This election can be made no later than the filing deadline of the income tax return for the taxation year during which the property is acquired. Similarly, section 130R134.1 of the Regulation respecting the Taxation Act, as proposed in Bill 90, tabled by the Government of Québec on May 4, 2021, allows for this election to also be made when the corporation has a permanent establishment in Québec.

Accelerated investment incentive property (AIIP)

To qualify, a property must be acquired and available for use after November 20, 2018, and meet the criteria in subsection 1104(4) of the Regulations.

AIIP available for use in the taxation year before 2028 are not subject to the half-year rule but benefit from a positive adjustment to the UCC used to calculate the CCA. Subsection 1100(2) ITR incorporates several rules to calculate the first-year allowance according to the CCA class:

- The general rule that applies for all CCA classes subject to subsection 1100(2) ITR (except classes 12, 13, 14, 15, 43.1, 43.2 and 53) allows for an increase in the UCC balance before CCA equal to 50% of the net additions (there is no addition for property acquired and available for use after 2023 and before 2028).

- Specific rules that apply to classes 43.1, 43.2 and 53, benefit from a 100% CCA of the cost of acquisition for property acquired after November 20, 2018, and available for use before 2024. A phase-out of the increased CCA is defined for each CCA class for property available for use after 2023 and before 2028.

- The half-year rule still applies to property that does not meet the criteria of the definition of “accelerated investment incentive property” from subsection 1104(4) ITR as well as property available for use after 2027.

In addition, specific rules are provided for CCA classes 13 and 14 in paragraphs 1100(1)(b) and (c) ITR. Therefore, for AIIP in CCA classes 13 and 14, the CCA will be equal to 150% of the CCA that would normally be calculated when the property becomes available for use before 2024 in the taxation year.

Calculation of line Maximum allowable CCA in the Federal column

For CCA classes other than 10.1, 13 and 14 or other than classes 24, 27, 29 and 34, the custom line 225, Cost of additions that are AIIP or ZEV included in the amount on line 203, allows you to enter the capital cost of qualified property. The amount on this line is calculated and equals the amount entered on line 203, Additions (property subject to subsection 1100(2) ITR), and is used to calculate the amount on the line UCC adjustment for AIIP and ZEV acquired during the year, which in turn, is taken into account when calculating the amount on the line Maximum allowable CCA.

For a CCA class 10.1, when the answer to the custom question Is the property AIIP? is Yes, the amount entered on the line Maximum allowable CCA will take into account the general rule for qualified property.

For CCA class 13, line 225, Cost of additions that are AIIP included in the amount on line 203, is updated and equals the amount on line 203, Current-year additions, property subject to subparagraph 1100(1)(b)(i) ITR. This line is used to calculate the amount added to the line Maximum allowable CCA taking into account clause 1100(1)(b)(i)(A) ITR.

For CCA class 14, when the answer to the custom question Is one of the properties an AIIP? is Yes, the amount entered on line 225, Cost of additions that are AIIP included in the amount on line 203, is calculated and equals the amount on line 203, Current-year additions. The latter is then used to calculate the amount on the line Maximum allowable CCA taking into account clause 1100(1)(c)(i)(A) ITR.

These calculations also apply to amounts in the Alberta column when the corporation has a permanent establishment in this province. Similarly, they also apply to the amounts in the Québec column, except for property in CCA classes 14.1, 44 and 50 that are properties qualified for the accelerated depreciation special rules in Québec.

Property qualifying for accelerated depreciation special rules in Québec

The Government of Québec further allows the increase to 100% of the depreciation for a property, acquired after December 3, 2018, and available for use before 2028, that is qualified intellectual property included in CCA class 14, 14,1 or 44 or, general-purpose electronic data processing equipment included in CCA class 50. For qualified property acquired and available for use in the taxation year, the CCA is equal to the capital cost of the acquired property.

A qualified intellectual property means property acquired after December 3, 2018, that is a patent or a right to use patented information, a licence, a permit, know-how, a commercial secret or other similar property constituting knowledge. The property must be acquired by the corporation in the course of a technology transfer or be developed by or on behalf of the corporation with a view to enabling the implementation of an innovation or invention with regards to its business. The expression “technology transfer” refers to the transmission, to a corporation, of knowledge in the form of know-how, techniques, processes or formulas. The process of implementing an innovation or invention as well as the implementation efforts of that innovation or invention must be made only in Québec.

Calculation of line Maximum allowable CCA in the Québec column

For CCA classes 14.1, 44 and 50, the custom line Capital cost of property qualified for the accelerated depreciation special rules in Québec included in the amount on line 203 allows you to enter the capital cost of qualified property. This line is used to calculate the amount to add to the line UCC balance for CCA calculation, according to the CCA class selected, and as a result, taking into account the rules for the calculation of the amount on the line Maximum allowable CCA. When CCA class 50 is selected, the amount on this line is calculated and equals the amount on line 203, Additions (property subject to subsection 1100(2) ITR).

For CCA class 14, when the answer to the custom question Is one of the properties acquired during the year a property that qualifies for the accelerated depreciation special rules in Québec? is Yes, the amount entered on custom line Capital cost of property qualified for the accelerated depreciation special rules in Québec included in the amount on line 203 is calculated and equals the amount on the line 203, Current-year additions. This amount is then used to calculate the amount on the line Maximum allowable CCA.

This section of the form is used to calculate the additional CCA amounts for qualified property in CCA classes 50 and 53. It includes two subsections:

- Additional CCA of 35%, for qualified property acquired after March 28, 2017, and before March 28, 2018, that became available for use in the current or preceding taxation year; and

- Additional CCA of 60%, for qualified property acquired after March 27, 2018, and before December 4, 2018, (or acquired after December 3, 2018, and before July 1, 2019, in accordance with an obligation in writing entered into before December 4, 2018, or for which the construction by or on behalf of the taxpayer began before December 4, 2018) that became available for use in the current or preceding taxation year.

Calculation of the amounts on lines “Half of the capital cost of qualified property that became available for use in the current taxation year” and “Capital cost of qualified property acquired in the current taxation year”

The amounts entered on these lines are calculated in the following situations:

- When information relating to qualified property is entered on copies of Schedule 8 WORKCHART ADD, Additions and Dispositions Workchart (Jump Code: 8 WORKCHART ADD) of an eligible class:

- If the acquisition date is after March 28, 2017, and before March 28, 2018, and is part of the corporation’s taxation year, the amount on the line Half of the capital cost of qualified property that became available for use in the current taxation year of subsection Additional CCA of 35%, will be equal to the total of 50% of the amounts entered on the line Adjusted capital cost – Québec in each copy of Schedule 8 WORKCHART ADD.

- The same calculation, if the acquisition date is after March 27, 2018, and before November 21, 2018 and is part of the corporation’s taxation year, will be performed on the line Half of the capital cost of qualified property that became available for use in the current taxation year in the Qualified property that was acquired after March 27, 2018, and before November 21, 2018 subsection under Additional CCA of 60%.

However, if the acquisition date is after November 20, 2018, and before December 4, 2018, and the CCA class is not a separate class for Québec, the following calculations will be performed in the Additional CCA of 60% - Qualified property that was acquired after November 20, 2018, and before December 4, 2018 section:

the amount on the line Capital cost of qualified property acquired in the current taxation year before December 4, 2018 that are not AIIP is equal to the total of the amounts entered on the line Adjusted capital cost – Québec in each copy of Schedule 8 WORKCHART ADD for property designated as not being an AIIP.

the amount on the line Capital cost of qualified property acquired in the current taxation year before December 4, 2018 that are AIIP is equal to the total of the amounts entered on the line Adjusted capital cost – Québec in each copy of Schedule 8 WORKCHART ADD for property designated as being an AIIP.

- When the amount on line 203, Additions (property subject to subsection 1100(2) ITR), is not calculated (because the property included in the class is not entered on copies of Schedule 8 WORKCHART ADD) and an amount is manually entered on that line:

if the taxation year begins after March 28, 2017, but before March 28, 2018, the amount on the line Half of the capital cost of qualified property that became available for use in the current taxation year of subsection Additional CCA of 35% will be equal to 50% of the amount entered on line 203, Additions (property subject to subsection 1100(2) ITR);

- if the taxation year includes March 28, 2018, a diagnostic will prompt you to enter an amount representing half of the capital cost corresponding to property acquired after March 27, 2018, and before November 21, 2018 and that became available for use in the current taxation year, on the line Half of the capital cost of qualified property that became available for use in the current taxation year in part Qualified property that was acquired after March 27, 2018, and before November 21, 2018 of subsection Additional CCA of 60% (the amount entered will then be automatically deducted from the amount in subsection Additional CCA of 35%);

- if the taxation year includes November 21, 2018, a diagnostic will prompt you to enter the capital cost amount corresponding to the property that was acquired after November 20, 2018, and before December 4, 2018, on one of the four lines in the Additional CCA of 60% - Qualified property that was acquired after November 20, 2018, and before December 4, 2018 subsection (50% of the amount entered will then be automatically deducted from the amount in subsection Additional CCA of 35%).

In all aforementioned cases, the answer to the question Does this class include property eligible for the additional capital cost allowance for Québec? is Yes. In all other cases, the answer will be Yes when you enter an amount on any line in the Additional capital cost allowance (CCA) for Québec section based on the corporation’s situation because the program cannot determine the acquisition date or the relevant capital cost for property eligible for the additional CCA for Québec.

Calculation of the lines “UCC of qualified property that became available for use in the preceding taxation year”

The amounts entered on these lines are calculated when rolling forward a client file in which an amount is entered on the line Half of the capital cost of qualified property that became available for use in the current taxation year and for qualified property that was acquired after March 27, 2018, and before November 21, 2018, or for qualified property that was acquired after November 20, 2018, and before December 4, 2018, on one of the four lines in the Additional CCA of 60% - Qualified property that was acquired after November 20, 2018, and before December 4, 2018 section. The amount will be calculated according to the data entered on the line Half of the capital cost of qualified property that became available for use in the current taxation year or Amount added to the UCC attributable to qualified property, in proportion to the amounts in the fields CCA claimed (amount on line 217) and UCC in the class before CCA.

In the Information Bulletin 2018-9 published on December 3, 2018, the Ministère des Finances du Québec announced that an additional capital cost allowance of 30% would be added for targeted property. The CCA amount corresponds to 30% of the amount deducted, for the previous taxation year, relating to the CCA with respect to targeted property. In addition, the Information Bulletin indicates that a separate class must be created for property of a same class that gives rise to the additional CCA.

Targeted property

Targeted property must be acquired after December 3, 2018. It can be property that is new at the time of its acquisition by the corporation and not property acquired from a person or partnership with which the corporation is not dealing at arm’s length. It must start being used within a reasonable period of time after being acquired and for at least 730 consecutive days. In addition, it must be used primarily in Québec and must not be property with regards to which the corporation was entitled to or could have been entitled to claim the additional capital cost allowance of 60%. The property must be:

- equipment used in manufacturing or processing (class 53) or, if acquired after 2025, property included in class 43, but that would have been included in class 53 had it been acquired in 2025;

- clean energy generation equipment (class 43.1 or 43.2); or

- general-purpose electronic data processing equipment and related operating system software (class 50).

In addition, a targeted property can be a qualified intellectual property (certain property in classes 14, 14.1 and 44).

The program considers that property included in classes 14, 14.1, 43.1, 43.2, 44, 50 and 53 acquired after December 3, 2018, is targeted property. If this is not the case, modify the answer to the question Is the property a property that qualifies for the additional CCA of 30% in Québec? in Schedule 8 WORKCHART ADD (Jump Code: 8 WORKCHART ADD). If you are not using Schedule 8 WORKCHART ADD, make the required adjustments in the Schedule 8 WORKCHART. For more details on eligible properties, consult the Information Bulletin 2018-9 published by the Ministère des Finances du Québec.

Steps to follow in order for the program to correctly calculate the CCA and the additional CCA in respect of targeted property

The question Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%?, located under the field “If yes, specify the property to be linked in order to transfer data” for classes 14.1, 43.1, 43.2, 44, 50 and 53, and in subsection “Québec only” located under subsection “Current-year additions” for a class 14, allows you to indicate if the class is a separate class for purposes of Québec calculations. The question Are properties entered in the Québec column eligible for the additional CCA of 30%? located under the question Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%? allows you to indicate if the CCA calculated for this class must be used the following year to calculate the additional CCA. Follow the instructions below in order for the program to correctly perform the calculations based on the corporation’s situation:

Situation number 1: All properties in the class are not targeted properties

If Schedule 8 WORKCHART ADD is used: No separate class is required, and the corporation is not entitled to the additional CCA. Create only one class and make sure that the answer to the question Is the property a property that qualifies for the additional CCA of 30% in Québec? determined by the program is “No” for all copies of Schedule 8 WORKCHART ADD of the class. Make sure that the answer to the questions Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%? and Are properties entered in the Québec column eligible for the additional CCA of 30%? in Schedule 8 WORKCHART is No.

If Schedule 8 WORKCHART ADD is not used: No separate class is required, and the corporation is not entitled to the additional CCA. Create only one class and make sure that the answer to the questions Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%? and Are properties entered in the Québec column eligible for the additional CCA of 30%? in Schedule 8 WORKCHART is No.

Situation number 2: All properties in the class are targeted properties

If Schedule 8 WORKCHART ADD is used: No separate class is required, and the corporation is entitled to the additional CCA for targeted property. Create only one class and make sure that the answer to the question Is the property a property that qualifies for the additional CCA of 30% in Québec? determined by the program is Yes for all copies of Schedule 8 WORKCHART ADD of the class. Therefore, the answer to the question Are properties entered in the Québec column eligible for the additional CCA of 30%? in Schedule 8 WORKCHART will be Yes. Make sure that the answer to the question Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%? in Schedule 8 WORKCHART is No. The program will use the CCA amount claimed on line 217 of the Québec column to calculate the additional CCA when rolling forward the client file.

If Schedule 8 WORKCHART ADD is not used: No separate class is required, and the corporation is entitled to the additional CCA for targeted property. Create only one class and make sure that the answer to the question Are properties entered in the Québec column eligible for the additional CCA of 30%? of Schedule 8 WORKCHART is Yes. Make sure that the answer to the question Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%? in Schedule 8 WORKCHART is No. The program will use the CCA amount claimed on line 217 of the Québec column to calculate the additional CCA when rolling forward the client file.

Situation number 3: The class contains targeted and non-targeted property

If Schedule 8 WORKCHART ADD is used: A separate class for purposes of the Québec calculations is required for targeted property, and the corporation is entitled to the additional CCA for targeted property. In a class, enter all properties in Schedule 8 WORKCHART ADD and make sure that the answer to the question Is the property a property that qualifies for the additional CCA of 30% in Québec? determined by the program is the correct one based on whether the property is targeted or not. Make sure that the answer to the questions Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%? and Are properties entered in the Québec column eligible for the additional CCA of 30%? in Schedule 8 WORKCHART is No. In that situation, all amounts for properties entered in Schedule 8 WORKCHART ADD will be transferred to the Federal and Alberta columns of Schedule 8 WORKCHART. Only the amounts for non-targeted property will be transferred to the Québec column. Then, create a new class, answer Yes to the question Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%? in Schedule 8 WORKCHART and enter only targeted property in Schedule 8 WORKCHART ADD. Make sure that the answer to the question Is the property a property that qualifies for the additional CCA of 30% in Québec? determined by the program is Yes for all copies of Schedule 8 WORKCHART ADD of this class. Make sure that the answer to the question Are properties entered in the Québec column eligible for the additional CCA of 30%? of Schedule 8 WORKCHART is Yes. The amounts in the Federal and Alberta columns of Schedule 8 WORKCHART will not be calculated for this copy of the class, and no amount should be entered in these columns. Only the amounts in respect of targeted property must be entered in the Québec column. The program will use the CCA amount claimed on line 217 of the Québec column to calculate the additional CCA when rolling forward the client file.

If Schedule 8 WORKCHART ADD is not used: A separate class for purposes of Québec calculations is required for targeted property, and the corporation is entitled to the additional CCA for targeted property. In a class, enter the amounts relating to targeted and non-targeted property in the Federal column of Schedule 8 WORKCHART. Make sure that the answer to the questions Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%? and Are properties entered in the Québec column eligible for the additional CCA of 30%? in Schedule 8 WORK Are properties entered in the Québec column eligible for the additional CCA of 30%?CHART is No. In the Québec column of Schedule 8 WORKCHART, enter only the amounts relating to non-targeted property, using an override. Then, create a new class, answer Yes to the questions Is this a separate class used solely for the Québec income tax return and relating to prescribed property qualifying for the additional CCA of 30%? and Are properties entered in the Québec column eligible for the additional CCA of 30%? in Schedule 8 WORKCHART and enter only the amounts relating to targeted property in the Québec column. The amounts in the Federal and Alberta columns of Schedule 8 WORKCHART will not be calculated for this copy of the class, and no amount should be entered in these columns. The program will use the CCA amount claimed on line 217 of the Québec column to calculate the additional CCA when rolling forward the client file.

See also

Additions and Dispositions Workchart and Class Property History Table

Statement Real Estate Rental Properties (Regulation 1100(11))

Leasehold Interests (Class 13)

Patents, Franchises, Concessions and Licences for a Limited Period (Class 14)

Prior Year Leasehold Additions

Passenger Vehicles (Class 10.1)

T2 Corporation – Income Tax Guide

CO-130.A - General Information

IN-191, Capital Cost Allowance in Respect of Property Acquired After November 20, 2018