Release Notes - CCH iFirm Taxprep T2 2023 v.1.0 (2023.10.35)

Our Support Centres are Going Digital: Emails are Now Our First Priority

As part of our transformation to digital support centres, we are pleased to announce that email inquiries will now be given first priority. This digital shift will allow us to process your requests even faster, and better meet your needs.

From now on, use emails instead of telephone to contact Customer Service and the Support Centre by including your account number and the name of your product in the subject line as well as detailed information in your email (form/line/diagnostic number, print screens, etc.) to get accelerated service!

Try our Knowledge Base!

Consult our Knowledge Base to quickly find the information you need!

Our Knowledge Base contains an array of articles answering technical and tax questions most frequently asked to Support Centre agents. All you need to do is enter a few key words and the articles display in order of relevance to provide you with valuable information that will accurately answer your questions.

About CCH iFirm Taxprep

Welcome to CCH iFirm Taxprep, the first cloud-based professional tax software in Canada.

CCH iFirm Taxprep runs in your Web browser, with nothing to install on your desktop. Therefore, all updates will be automatically deployed during tax season.

Please note that CCH iFirm Tax is only supported on the Google Chrome and the Microsoft Edge (based on Chromium) Web browsers.

CCH iFirm Taxprep is bilingual and provides you with:

- Most robust tax calculations of the industry, imported from the Taxprep software programs;

- Comprehensive diagnostics with audit trail of user reviewed diagnostics;

- Ability to navigate through cells with data entered in the year;

- Ability to add review marks and comments;

- Intuitive user interface;

- and many more other features.

If you want to learn about the new non-tax related features delivered with this new CCH iFirm Taxprep version, consult the Technical Release Notes.

About CCH iFirm Taxprep T2

With CCH iFirm Taxprep T2, have the most comprehensive collection of corporate tax forms available, as well as tools designed to address complex T2 preparation requirements. CCH iFirm Taxprep T2 also provides you with:

- the possibility of attaching supporting documents to electronically transmitted returns;

- GIFI data transfers.

Taxation Years Covered

CCH iFirm Taxprep T2 2023 v.1.0 is designed to process corporate tax returns with taxation years beginning on or after January 1, 2021, and ending on or before October 31, 2023.

Overview - Version 1.0

CCH iFirm Taxprep T2 2023 v.1.0 includes several technical and tax changes. Here is a summary of the main topics addressed in this document.

Electronic transmission for Schedule 89 and Form T2054

The electronic transmission of Schedule 89 and Form T2054 has been added. These transmissions are carried out separately from the T2 return electronic transmission. You will need an EFILE number to do these transmissions. For more information, consult the notes relating to these subjects.

New Form T2183

Form T2183 has been added to authorize a person to electronically file special elections in the name of the filing corporation. For more information, consult the note relating to this subject.

Improve Your Productivity

Federal

Schedule 89, Request for Capital Dividend Account Balance Verification

Electronic filing is now available for Schedule 89.

Schedule 89 is transmitted separately from the T2 return.

Section Electronic filing has been added. The electronic status will be displayed at the end of this section. When the status is at Eligible, you can transmit Schedule 89. Refer to the diagnostics to complete the schedule correctly.

For more information on electronic filing, consult the help topic on Schedule 89 and the note relating to the transmission of Schedule 89 in the June 2, 2023 Release section of the CCH iFirm Tax Releases Notes.

T2054, Election for a Capital Dividend Under Subsection 83(2)

Electronic filing is now available for Form T2054.

Form T2054 is transmitted separately from the T2 return.

To allow you to select the form for electronic filing, section Form T2054 filing methods has been added at the top of the form.

The instructions section has been modified so that the correct information for the selected filing method is displayed.

Section Electronic filing has also been added. The electronic status will be displayed at the end of this section. When the status is at Eligible, you can transmit Form T2054. Refer to the diagnostics to complete the form correctly.

For more information on electronic filing, consult the help topic on Form T2054 and the note relating to the transmission of Form T2054 in the June 2, 2023 Release section of the CCH iFirm Tax Releases Notes.

Preparer profiles

EFILE tab

In the Canada Revenue Agency subsection of the EFILE tab, the boxes Select Forms T2054 for electronic filing and Select Schedule 89 for electronic filing have been added to allow you to select Form T2054 and/or Schedule 89 for electronic filing.

Please note that the boxes of this subsection will be checked by default if you create a new preparer profile or if you convert an existing profile.

Authorization Forms tab

The Electronic filing subsection has been added to the MR-69 – Authorization to communicate information or power of attorney section. This new subsection allows you to select electronic filing for all MR-69 forms that are applicable.

Note that the box in that subsection will be selected by default if you create a new preparer profile or if you convert an existing profile.

EFILE Information

Sections Schedule 89 and Schedule 89 – Docs have been added to the form. You will find key information regarding the electronic filing of Schedule 89 and its supporting documents as well as the information required to correct the supporting documents to be electronically filed, in the event they are rejected.

Section T2054 has also been added. You will find key information regarding the electronic filing of this form. The information required to correct the form and the supporting documents to be electronically filed, in the event the form is rejected, will be displayed on the copy of Form T2054, as applicable.

For more information, consult the note relating to the transmission of supporting documents of Schedule 89 and Form T2054 in the June 2, 2023 Release section of the CCH iFirm Tax Releases Notes.

A section named MR-69 was added to the form and contains key information regarding the electronic filing of every MR-69 forms for the corporation of the active client file. The transaction history information and the information required to correct the form for electronic transmission purposes, in the event the form is rejected, are displayed on the corresponding copy of the MR-69 form.

Québec

MR-69, Authorization to Communicate Information or Power of Attorney

Form MR-69 can now be submitted electronically. As opposed to the authorization transmission to the federal government, which does not require proof of signature with the electronic transmission, Revenu Québec requires that a PDF document containing all four pages of the signed Form MR-69 is transmitted along with the electronic transmission. In the case of an electronically signed document, five pages are allowed.

When the signing officer is not one of the executive officers (e.g., president, vice president, secretary, or treasurer), an additional document supporting the designation of the signatory must also be attached to the electronic transmission. If there are multiple documents, they should be grouped into a single file in PDF, JPEG or TIFF format.

A maximum of two documents can be attached to the client file and filed with the transmission.

A custom checklist has been added to Form MR-69 to help you prepare and electronically transmit it. When the answer to all statements of both steps is Yes, the form meets the requirements of Revenu Québec and can be submitted. This prevents for getting an error code at the time of the electronic transmission.

The first step in the list helps you complete the form correctly before printing it, so that the printed copy meets the requirements of Revenu Québec and contains a 2D bar code when the copy is signed by the taxpayer or their representative.

The second step in the list covers the requirements that should be met to be able to electronically transmit the form and the attached document(s).

The electronic transmission status of the form can be found at the end of the checklist. When the status is Eligible, you can transmit the MR-69 form and the attached documents.

For more information and clarification on the checklist, consult the help topic on the MR-69 form.

New Forms

Federal

T2183, Information Return for Electronic Filing of Special Elections

Form T2183 has been added to the program to authorize an electronic filer to electronically file special elections in the name of the filing corporation. The special elections are indicated in Part 3 of the form and are:

-

Form T217, Election or Revocation of an Election to use the Mark-to-Market Method

-

Form T2054, Election for a Capital Dividend Under Subsection 83(2)

-

Form T2SCH89, Request for Capital Dividend Account Balance Verification

Take note that only special elections for Form T2054 , Election for a Capital Dividend Under Subsection 83(2) and Schedule 89, Request for Capital Dividend Account Balance Verification are supported by the program.

This is a multicopy form, and you must complete a copy of this form for each special election or amendment. More precisely, for each Schedule 89 and copy of Form T2054 with the Eligible electronic filing status, you must complete an equal number of copies of Form T2183. An authorized signing officer of the corporation must sign the copy(ies) of Form T2183 before Schedule 89 or Form 2054 are filed. To print the form, use the Print Form command (Ctrl + Shift + p). Take note that the data from this form is not included in the T2 return.

Do not send Form T2183 unless the CRA requires you to do so. Keep a copy of the signed form in your files for six years.

The copy of the form is applicable when a third party completes it and you have activated the box for Schedule 89 or Form T2054 in section 3. In addition, at the end of section 3, the custom line For internal use: If you wish, you can add a description that will identify the copy of the T2183 form has been added to help track the copies of Form T2183.p

Deleted Forms

Ontario

-

Schedule 504, Ontario Resource Tax Credit

-

Schedule 552, Ontario Apprenticeship Training Tax Credit

Updated Forms

* Note that form titles followed by an asterisk (*) have been updated according to the most recent version issued by the applicable tax authority.

Federal

Corporate Identification and Other Information

The Japanese yen has been added to the list of currencies that can be selected on line 079, If an election was made under section 261, state the functional currency used, when a return is prepared using a functional currency.

The Alberta Tax and Revenue Administration (ATRA) has indicated that they will not accept, for the time being, the Japanese yen as a functional currency when filing AT1 returns. If the corporation is using the Japanese yen as a functional currency and it must file an AT1 return with the ATRA, that return should be filed using Canadian dollars.

The same is also true for Revenu Québec. The Agency does not accept the Japanese yen as a functional currency when filing CO-17 returns. If the corporation is using the Japanese yen as a functional currency and it must file a CO-17 return with Revenu Québec, that return should be filed using Canadian dollars.

Tax Preparer’s Profile

PROFILE tab

EFILE tab

Check boxes Using an electronic signature method on Form T106, Using an electronic signature method on Form T1134 and Using an electronic signature method on Form T1135 have been removed from the Tax Preparer’s Profile.

Schedule 200, T2 Corporation Income Tax Return*

In Part Identification, the Japanese yen has been added to the list of currencies that can be selected on line 079 when a return is prepared using a functional currency.

Under Part Refundable dividend tax on hand, lines 460, 465 and 480 as well as lines A through I have been removed, as they relate to the amount in the RDTOH account before 2019.

Finally, in addition to the EFILE number indicated on line 920 that serves as a first identifier, line 925, RepID, has been added and is used as a second identifier for tax preparers who prepare returns for a fee. The CRA has indicated that the RepID entered should be the same that you or your firm provided during the registration or the renewal process for the EFILE number, regardless of who is preparing or transmitting the return. Currently, this field is optional and can be left blank. If entered, the RepID will be transmitted electronically with the return. The CRA also indicated that this is simply an additional mechanism to ensure that the users of EFILE services have been suitably screened.

When opening a return prepared with a prior version of CCH iFirm Taxprep T2, the amount calculated or entered by override on lines 520 and 535 are retained as inputted values.

Schedule 3, Dividends Received, Taxable Dividends Paid, and Part lV Tax Calculation*

Schedule 5, Tax Calculation Supplementary – Corporations*

Line 404, Ontario resource tax credit (from Schedule 504), has been removed from the schedule. When opening a return prepared with a prior version of CCH iFirm Taxprep T2, if an amount was entered on this line, it will not be retained.

Line 454, Ontario apprenticeship training tax credit (from Schedule 552), has been removed from the schedule. When opening a return prepared with a prior version of CCH iFirm Taxprep T2, if an amount was entered on this line, it will not be retained.

Line 623, Manitoba refundable odour-control tax credit for agricultural corporations (from Schedule 385), has been removed from the schedule. When opening a return prepared with a prior version of CCH iFirm Taxprep T2, if an amount was entered on this line, it will not be retained.

Line 326, Manitoba refundable rental housing construction tax credit (from Schedule 394), has been removed from the schedule. When opening a return prepared with a prior version of CCH iFirm Taxprep T2, if an amount was entered on this line, it will not be retained.

Line 884, Certificate number has been added. This line allows you to enter the British Columbia clean buildings tax credit certificate number when you have only one certificate.

Line 696, Yukon mining business carbon price rebate (from Schedule 444) has been added. This line is calculated from line E of Schedule 444.

Schedule 8 WORKCHART, Capital Cost Allowance (CCA) Workchart

For CCA class 10.1, the part Proceeds of disposition for a passenger vehicle (DIEP in a prior taxation year only) has been added to calculate the amount to enter on line 207, Proceeds of disposition, in the case of the disposition of a passenger vehicle that is a DIEP. The following fields have been added:

-

Proceeds of disposition

-

Cost of the passenger vehicle

-

Original capital cost (line 203 in the taxation year of the acquisition)

-

Government assistance received or repaid

-

Does the corporation not deal at arm's length with the purchaser?

-

Applicable proceeds of disposition

When the date of disposition is part of the taxation year and the answer to the question Was the property a DIEP in a prior taxation year? is Yes, complete the fields under the Part Proceeds of disposition for a passenger vehicle (DIEP in a prior taxation year only). The amount on line 207, Proceeds of disposition, is equal to the amount calculated on the line Applicable proceeds of disposition when this amount is greater than the UCC available to calculate the recapture of CCA for a passenger vehicle that is a DIEP under subsection 13(2) ITA. In other situations, line 207 is calculated to 0.

When opening a return prepared with a prior version of CCH iFirm Taxprep T2, if an amount is entered on line 207 and the answer to the question Was the property a DIEP in a prior taxation year? is Yes, the amount on line 207 will be retained on the new line Applicable proceeds of disposition as an overridden value.

When rolling forward a file in which a passenger vehicle has been acquired in the taxation year and in which the answer to the question Is the property a designated immediate expensing property (DIEP) for the taxation year? is Yes, the amount rolled forward on the new line Original capital cost (line 203 in the taxation year of the acquisition) corresponds to the amount entered on line 203, Current-year addition. This amount will then be rolled forward until the vehicle is disposed of.

In addition, for CCA classes other than 10.1, 13 and 14, line Negative UCC (closing) has been added under line 220, UCC (closing), and is calculated when the amount on line 217, CCA claimed, is greater than the amount on line UCC balance (before immediate expensing). This situation usually happens, for a CCA class with a CCA rate of 100%, when the UCC balance at the start of the taxation year on line 201 is lower than the negative adjustments and transfers on line 205 (primarily the ITC on property acquired in a prior taxation year) that do not affect the adjustments to the UCC under subsection 1100(2) ITR for acquisitions made in the current taxation year.

In such a case, the UCC balance at the end of the taxation year on line 220 may be negative when the CCA is fully claimed on line 217. However, for the various tax authorities, the UCC balance at the end of the year cannot be negative. Therefore, this negative amount must either be applied to another CCA class with the same number or carried forward to the next taxation year.

When a negative amount is calculated or entered on this new line, the amount is rolled forward to line 205, Adjustments and transfers not affecting the adjustments under subsection 1100(2) ITR. If you do not wish to roll forward this amount, enter “0”, using an override.

Schedule 17, Credit Union Deductions*

Former line 3F relating to the number of days in the taxation year before January 1, 2021, has been removed from the schedule. When opening a return prepared with a prior version of CCH iFirm Taxprep T2, if an amount was entered on this line, it will not be retained.

Schedule 27, Calculation of Canadian Manufacturing and Processing Profits Deduction*

For the qualified zero-emission technology manufacturing (ZETM) activities (Parts 14 to 16), the following modifications have been made:

-

Former line 14C has been removed, and the amount on line ZETM profits now equals the amount on line 14A when the ratio calculated on line 14B is equal or greater than 0.9.

-

Lines 15A and 15B have been removed, and line 305 is now an input line that corresponds to the portion of the capital cost from line 140 in Part 4 that relates to property used directly in qualified ZETM activities of the corporation during the year, in accordance with the ZETM capital cost definition.

-

Line 16C has been removed, and the amount on line 306 now equals the total amount of lines 16A and 16B, in accordance with the ZETM cost of labour definition.

When opening a return prepared with a prior version of CCH iFirm Taxprep T2:

-

The amount entered by override on former line 14C will not be retained.

-

When the amount on line 305 is entered by override, this amount will be retained as an input value. Otherwise, the amount entered on line 15B will be retained on line 305 as an input value.

-

When the amount on line 306 is entered by override, this amount will be retained. Otherwise, the amount from line 16C will be retained on line 306.

Schedule 38, Part VI Tax on Capital of Financial Institutions*

Schedule 53, General Rate Income Pool (GRIP) Calculation*

Schedule 67, Canada Recovery Dividend*

Note 1 in Part 1 has been removed. Consequently, the calculation that makes the amount zero on line 120, Income deduction of the corporation, when the total of column 3 of the table in Part 1 exceeds $1 billion, has been corrected. Thus, if the amount on the line Total income deduction allocated to members of the related group is greater than $1 billion, the amount allocated to the corporation on line 120 will not be deemed to be nil.

Schedule 68, Additional Tax on Banks and Life Insurers*

Schedule 141, General Index of Financial Information (GIFI) – Additional Information*

In Part 1, the question Were financial statements prepared? on line 111 has been changed to Can you identify the person specified in the heading of Part 1?

In Part 2, line 198 has been replaced by lines 300, 301, 302 and 305. However, clarifying details must now be added if the Other option is used. Two new options have been added to lines 303 and 304: Provided accounting services and Provided bookkeeping services. You must now choose at least one option even when the answer on line 111 is No. When opening a return prepared with a prior version of CCH iFirm Taxprep T2 in which options 1, 2 or 3 had been selected, these options will be retained on lines 300 to 302. However, if you had selected option 4, Other, the required clarifying details should be added. Please make sure you select every relevant option.

In Part 4, lines 104 and 107 must be answered even if the answer on line 101 is No.

Finally, in Part 5, line 110 has been replaced by lines 310 to 314. Three new options have been added to lines 312, 313 and 314. When opening a return prepared with a prior version of CCH iFirm Taxprep T2 in which option 1 had been selected, that option will be retained on line 311. However, if option 2 had been selected, that option will be retained on line 310. Please make sure you select every relevant option.

Schedule 556, Ontario Film and Television Tax Credit*

Inducement, Inducement calculation workchart

The line New Brunswick film tax credit has been removed. This line applied to salaries paid prior to 2020. It is no longer possible to enter such tax years in this version of CCH iFrim Taxprep T2.

T106 Summary, Information Return of Non-Arm’s Length Transactions with Non-Residents

The question Are you planning on using an electronic signature method on Form T106? has been removed in the Electronic Filing section. The CRA has requested that the mention “FOR ELECTRONIC SIGNATURE ONLY – DO NOT SEND BY MAIL TO CRA” be removed when the form is sent to obtain an electronic signature.

T217, Election, or Revocation of an Election, to Use the Mark-to-Market method 217*

T1134, Information Return Relating to Controlled and Non-Controlled Foreign Affiliates

The question Are you planning on using an electronic signature method on Form T1134? has been removed in the Electronic Filing section. The CRA has requested that the mention “FOR ELECTRONIC SIGNATURE ONLY – DO NOT SEND BY MAIL TO CRA” be removed when the form is sent to obtain an electronic signature.

T1135, Foreign Income Verification Statement*

The question Are you planning on using an electronic signature method on Form T1135? has been removed in the Electronic Filing section. The CRA has requested that the mention “FOR ELECTRONIC SIGNATURE ONLY – DO NOT SEND BY MAIL TO CRA” be removed when the form is sent to obtain an electronic signature.

Federal Tax Instalments

Line Additional tax on personal services business income has been added in Part Instalment base calculation.

AgriStability and AgriInvest – Programs – Prince Edward Island*

Québec

CO-156.EN, Agreement Concerning Regional Limits Respecting the Additional Deduction for Transportation Costs of Small and Medium-Sized Manufacturing Businesses*

CO-156.TR, Additional Deduction for Transportation Costs of Small and Medium-Sized Manufacturing Businesses*

The lines related to the calculation of the additional deduction rate for taxation years ending after June 4, 2014, have been removed from Part 4.

The lines related to the area in respect of which the additional deduction is being claimed for taxation years starting before January 1, 2015, have been removed from Part 3.3.

When opening a return prepared with a prior version of CCH iFirm Taxprep T2, the choices indicated on lines 32, 33 and 34 will not be retained.

CO-156.TZ, Additional Deduction for Transportation Costs of Small and Medium-Sized Businesses Located in a Special Remote Area*

CO-1029.8.33.6, Tax Credit for an On-the-Job Training Period

The question Are the expenses entered on this copy of the form incurred after April 30, 2022? has been added in the Eligible expenses section of Form CO-1029.8.33.6 PARTS 2 to 7. You must answer the question when the training period begins before March 26, 2021, and ends after April 30, 2022, so that lines 56 or 74 are calculated accurately and the diagnostics of columns R or JJ are displayed correctly, as the case may be.

CO-1029.8.36.EL, Tax Credit for Book Publishing

Following the announcement of the 2023–2024 budget tabled on March 21, 2023, the Government of Quebec increased the refundable tax credit for book publishing by raising the limit on eligible labour expenditure attributable to preparation costs and digital version publishing costs.

To reflect these changes, two new lines have been added in Section 2 to indicate whether the application for an advance ruling or for a qualification certificate was filed with SODEC before or after March 21, 2023. This will allow us to use the correct rates in the following sections: 4.3, 5.1 and 5.3. Note that these changes only appear on the screen and not when printing.

CO-1029.8.36.II, Tax Credit for Investment and Innovation

The following changes have been made to the list of geographic codes on line 14a.1:

-

Code 88015 La Morandière and code 88010 Rochebaucourt have been replaced by code 88012 La Morandière-Rochebaucourt.

-

The name of the municipality previously associated to code 56010, Saint-Georges-de-Clarenceville, has been replaced by Clarenceville.

CO-1029.8.36.XM, Tax Credit for the Production of Multimedia Events or Environments Presented Outside Québec

In its 2023-2024 budget tabled on March 21, 2023, the Québec government announced an enhancement of the refundable tax credit for the production of multimedia events or environments presented outside Québec. According to the additional information, there will be an increase in the limit on qualified labour expenditure. As such, the tax legislation will be amended so that the percentage of 50% used to calculate the limit will be raised to 60% for advance rulings or applications for a qualification certificate that are filed with the SODEC after March 21, 2023.

Therefore, we have added the custom box Limit based on the cumulative production costs: select the box if an advance ruling or a qualification certificate application was filed with the SODEC after March 21, 2023 in Part 2 so that the timing of the application can be specified. If so, in Part 4.3, the applicable rate for the limit will be raised to 60%. If not, the applicable rate will remain at 50%. Please note that, since this is a prescribed form, the rate displayed on the printout will be 50% in all cases. However, the amount on line 153, Overall limit based on the cumulative production costs, will be calculated based on the answer to the new question.

Ontario

Schedule 500, Ontario Corporation Tax Calculation*

The lines relating to the number of days in the tax year before 2020 have been removed from Parts 2 and 4. When opening a return prepared with a prior version of CCH iFirm Taxprep T2, no value related to the removed lines will be retained.

British Colombia

Schedule 423, British Colombia Production Services Tax Credit*

Schedule 428, British Columbia Training Tax Credit*

Schedule 430, British Columbia Shipbuilding and Ship Repair Industry Tax Credit*

Alberta

AT1 Schedule 1, Alberta Small Business Deduction*

Following the update of this schedule, the presentation of element (ii) Business Limit Reduction in section AREA B – Determination of the Value for Line 015 has changed. The first line (c) applies to a taxation year that begins before April 7, 2022, and the second line (c) applies to a taxation year that begins after April 6, 2022. Although the presentation has changed, the end result remains the same. When opening a return prepared with a prior version of CCH iFirm Taxprep T2, if an override had been made to one of the lines (c), it would not be retained.

AT1 Schedule 13, Alberta Capital Cost Allowance (CCA)*

The former column 4, Cost of acquisitions from column 3 that are Accelerated Investment Incentive Property (AIIP), has been removed, and line 029 has been moved to the new column 14.

The following columns and line numbers have been added:

-

Column 4, Cost of acquisitions from column 3 that are designated immediate expensing property (DIEP) (line 039)

-

Column 9, Proceeds of disposition of the DIEP (line 041)

-

Column 11, UCC of the DIEP (line 043)

-

Column 12, Immediate Expensing (line 045)

-

Column 13, Cost of acquisitions on remainder of Class

-

Column 14, Cost of acquisitions from column 13 that are accelerated investment incentive properties (AIIP) or properties in Classes 54 to 56 (line 029)

-

Column 15, Remaining UCC

All the other columns have been renumbered accordingly.

When the AT1 return is filed and the AT1 Schedule 13 is applicable, lines 039, 041, 043 and 045 are included in the Net File transmission or the RSI printing.

Alberta Schedule 29 Listing, Listing of Innovation Employment Grant Projects Carried out in Alberta*

Alberta Corporate Income Tax – Filing Exemption Checklist*

The Alberta government has replaced the AT100 form, Preparing and Filing the Alberta Corporate Income Tax Return, with the Alberta Corporate Income Tax - Filing Exemption Checklist form. The calculations of this form and the impacts on the program remain the same, and only esthetic changes were made. Keep this form in your files and no matter the situation of the corporation, you must not send it to the TRA.

Saskatchewan

Schedule 411, Saskatchewan Corporation Tax Calculation*

The lines for the calculation of the Saskatchewan tax at the lower rate for tax years ending before October 1, 2020, have been removed from Part 3.

In addition, the line 3B has been added in Part 3 to calculate the Saskatchewan tax at the lower rate for tax years ending after June 30, 2024.

Manitoba

Schedule 387, Manitoba Small Business Venture Capital Tax Credit*

Yukon

Schedule 443, Yukon Corporation Tax Calculation*

Schedule 444, Yukon Business Carbon Price Rebate

The Yukon business carbon price rebate now includes the carbon price rebate for the Yukon mining businesses. This rebate is structured in the same way as the existing business rebate. It can be claimed by a business whose taxation year ends after 2022 and that is using eligible Yukon mining assets.

Parts 1, 2 and 3 have been added to Schedule 444 to calculate the carbon price rebate to Yukon mining businesses. The calculated rebate is then reported on line 696 of Schedule 5.

Parts 1 and 2 of the previous version have been moved to Parts 4 and 5 of the current Schedule.

Northwest Territories

Schedule 461, Northwest Territories Corporation Tax Calculation*

Nova Scotia

Schedule 341, Nova Scotia Corporate Tax Reduction for New Small Businesses*

Schedule 346, Nova Scotia Corporation Tax Calculation*

The lines relating to the number of days in the tax year before 2020 have been removed from Part 2. When opening a return prepared with a prior version of CCH iFirm Taxprep T2, no value related to the removed lines will be retained.

Schedule 353, Nova Scotia Financial Institutions Capital Tax Agreement Among Related Corporations*

Prince Edward Island

Schedule 322, Prince Edward Island Corporation Tax Calculation*

Line 2 relating to the number of days in the taxation year before January 1, 2021, has been removed from the schedule. When opening a return prepared with a prior version of CCH iFirm Taxprep T2, if an amount was entered on this line, it will not be retained.

Corrected Calculations

The following problems have been corrected in version 2023 1.0:

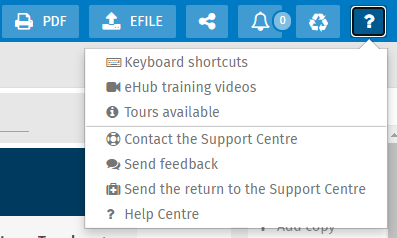

Where to Find Help

This version provides the following help resources:

- List of available keyboard shortcuts;

- eHub training videos.

To access the Help or to submit a suggestion or idea regarding the product, click the following icon in the top right portion of the screen:

Note that the CCH iFirm Taxprep T2 e-Bulletin notifies you each time an updated or new form is made available in a program update.

How to Reach Us

Technical and Tax support Hours

Monday to Friday: 8:30 a.m. to 8:00 p.m. (EST)

Toll Free: 1-800-268-4522

E-mail: csupport@wolterskluwer.com